People who own a created household may be used to spending way more, nonetheless don’t have to.

Despite prominent imagine, owning a created household does not have any so you can indicate high pricing and you will prepayment penalties. The value and you can top-notch these types of home is actually improving, and generally are the credit options. In fact, for many who individual this new land together with manufactured household, the fresh prices and fees are nearly same as a normal solitary-family home. Adhere these half a dozen information whenever money a created house.

1. Very own the land

For individuals who purchased a produced family, maybe you are financially alert and you can in charge. Chances are, you wanted to prevent getting in more than your face with an enthusiastic pricey home. While to acquire assets may be a little pricier up-front side, it’s actually the new shorter-costly channel for people who factor in the price so you can lease and you will the higher pricing given to own home financing. You’ll find residential property-and-household packages available to choose from and you will, after you very own brand new belongings therefore the family, chances are the value of your house increase.

dos. Pick re-finance

Think about this: For those who got the new builder’s otherwise seller’s common resource, there is the solution to refinance from the jawhorse. Which route could help you get this money even more individualized so you can suit your need.

Refinancing a created residence is quite common throughout the mortgage community. One type of refinancing exchange is actually cash-aside, then you can also be refinance and use that cash to build like improvements (hello the new kitchen area!). However,, in these products, the brand new costs offered is higher than a rate-and-name re-finance. Benefit from the fresh new improved kitchen area (or similar improve) but getting informed: If you opt to capture cash out, you have got to hold off six months immediately after purchasing the house-or, you could gain benefit from the rates-and-identity re-finance the following day and spend less over the life of one’s mortgage.)

step three. Enable it to be a great fifteen-season name

Typically, the danger towards the a beneficial 15-seasons financial identity is much all the way down and cost much more glamorous than many other offered identity lengths. Those who are three to four decades to your a 30-season label that have a speeds from seven9% was thrilled to find that they can refinance for the an effective fifteen-season term in addition to their payment ount. In this situation, the newest debtor may continue to have a similar fee but, in lieu of buying a unique twenty-six ages, they only possess fifteen years remaining. Where you’ll find solutions, there can be the possibility.

4. See if your qualify for HARP and streamline money

If your brand new mortgage are FHA or traditional, you could be eligible for these types of unique apps. Remember that only a few lenders give such apps. Unsure for those who have an excellent HARP Qualified Financing? Learn here that is where to find out if you reside detailed. In the event your residence is detailed, you may also qualify for an excellent HARP financing. For people who currently have a keen FHA mortgage, look at your month-to-month report to see if it’s indexed because FHA. While entitled to these types of apps, you will need to take advantage of all of them and the extra money they can installed your wallet.

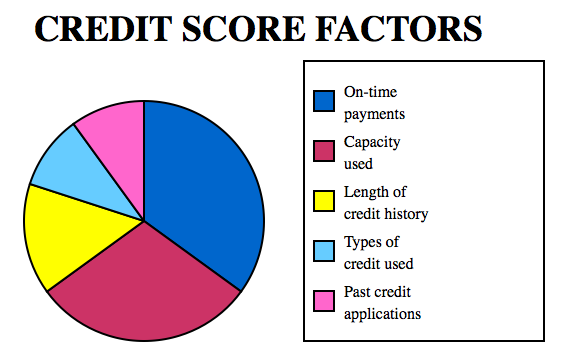

5. Get aquainted with your credit rating

If at all possible, keep your own complete borrowing put less than 29% of your borrowing limit. This matchmaking (shown as the a share) between your quantity of a fantastic stability on any credit cards separated from the amount of for every single card’s restriction is named your credit utilization ratio. You want a much deeper cause? Come across an effective analogy right here out-of how borrowing utilization ratios are calculated.

six. Have some money in the financial institution

Try to keep some funds during the coupons and avoid mobile fund between accounts. Underwriters basically want to see that your particular deals try steady and you may will not vary much. Plenty of transfer pastime may cause an underwriter to inquire about for a papers walk-proof new transmits and you will where the funds originated. One possibility you have got to legitimize your money work within the your own favor.

Were created property could have a credibility to carry large pricing and you may prepayment penalties, but one to belief is fast changing. Since home loan industry progresses, a lot more potential try starting to possess sensible are built a home loan.

Recent Comments